Economists for CoBank sounded the alarm that challenging times lie ahead for both the agriculture and the broader economy as the COVID-19 pandemic plays out across the country.

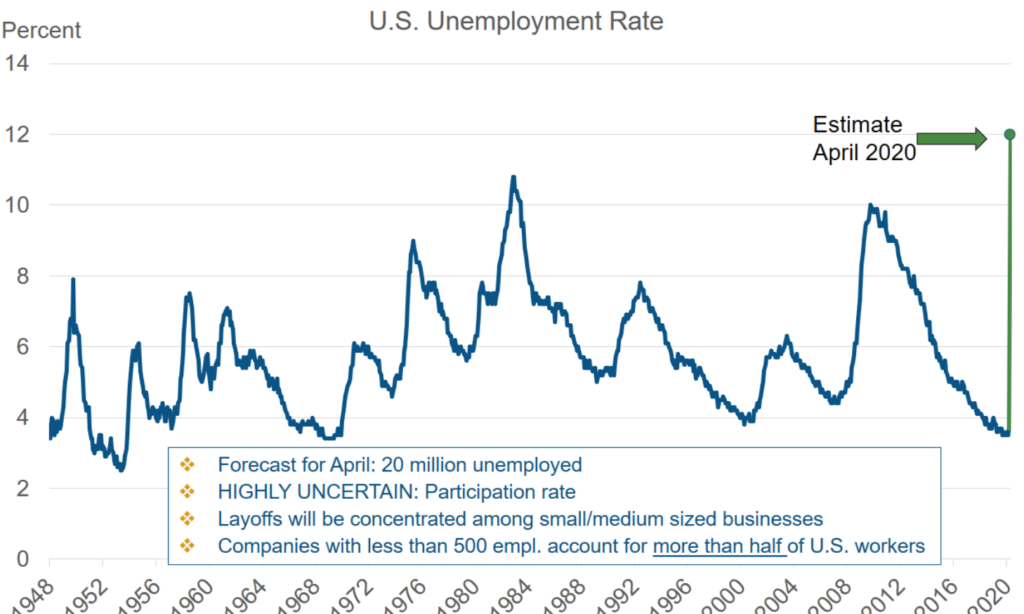

The forecast for various segments of the agriculture economy was difficult to predict considering just how large the economic dislocation stemming from the COVID-19 crisis is anticipated to be. Speaking about job losses and the April unemployment rate, Dan Kowalski, vice president of CoBank’s Knowledge Exchange said, “There’s just no way to compare this to any of the previous downturns.”

Unemployment claims last week totaled as much as six times higher than at the height of the Great Recession in 2008-2009. Nationwide, the April unemployment rate is anticipated to be nearly 12 percent. Kowalski also noted that unlike previous downturns, the current situation is anticipated to hit small and medium-sized businesses the worst as restaurants and other service providers are forced to close to help slow the spread of the virus. Future GDP projections are also in flux, with estimates from different banks and financial institutions varying widely.

For agriculture markets, variability and uncertainty is also the leading factor with some sectors helped and others hit hard by the crisis. Even sectors currently seeing positive movement are expected to be hit hard as the infection moves across the country. In many areas, meat case prices have been helped by a spike in consumer demand, but overall prices for beef are expected to drop as restaurants and food-service orders collapse.

Other commodities like wheat have also been helped by a demand spike as consumers make virus-driven purchasing decisions.

“We also see odd market demand with consumers buying more flour and bread,” said Tanner Ehmke, manager at the Knowledge Exchange. Ehmke also said wheat prices have been helped by major purchases from China as the nation works to adhere to the phase-one trade deal is has with the U.S.

The change in consumer food purchasing habits is anticipated to be an ongoing source of uncertainty and of shifting market dynamics. Almost overnight, grocery stores have gone from providing nearly 48% of America’s food, to nearly 90%. Kowalski noted this accounts for the shortages of various foods on grocery shelves and predicted that the tension in the supply chain would abate in the coming days as processors and retailers adjust to this new reality.

Corn markets have also taken a hit in recent weeks. Ehmke is concerned about future prices, noting that USDA’s most recent Prospective Plantings report shows corn acres will be up significantly (3 million acres from Feb.) in 2020 to an anticipated 97 million acres. That, coupled with cratering demand for ethanol as a result of a significant drop in gasoline demand and prices could spell trouble for corn in the coming months.

Corn markets have also taken a hit in recent weeks. Ehmke is concerned about future prices, noting that USDA’s most recent Prospective Plantings report shows corn acres will be up significantly (3 million acres from Feb.) in 2020 to an anticipated 97 million acres. That, coupled with cratering demand for ethanol as a result of a significant drop in gasoline demand and prices could spell trouble for corn in the coming months.

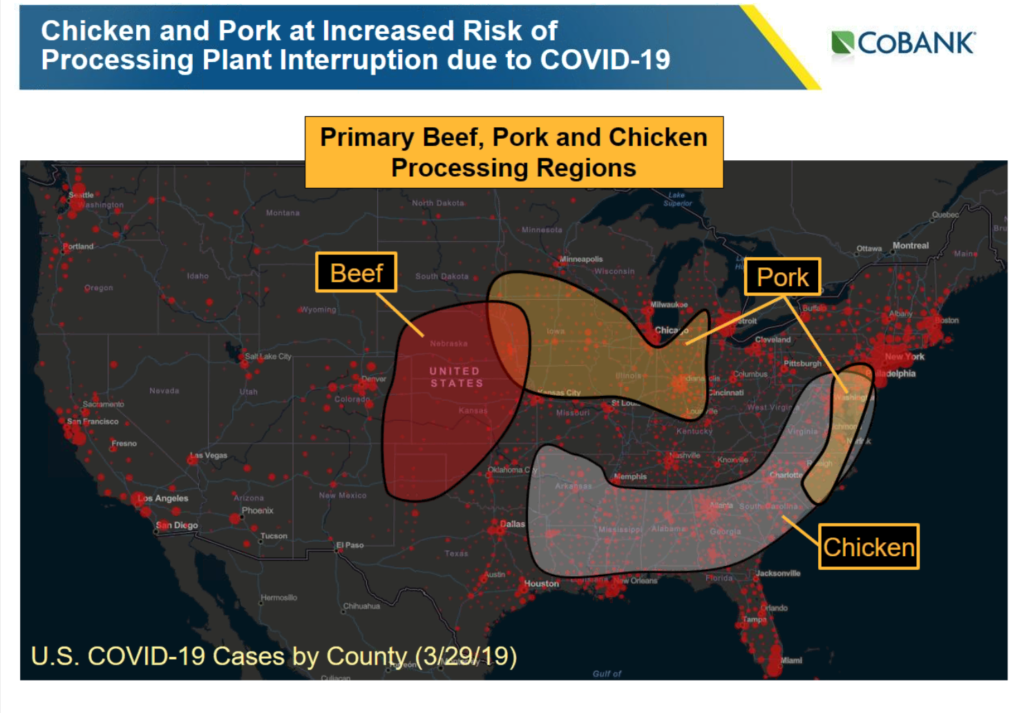

More trouble may be on the horizon for the meat sector as the COVID-19 virus makes its way across the country and causes further closures at meat processing plants. The group noted that overall monthly meat exports are up 16%, led by pork exports at an increase of 39% as China steps up buying. This strong export performance will need to continue if domestic meat prices are to fare well in the coming weeks.

Already, plants in New York and Maryland have closed as employees become sickened by COVID-19. Greeley’s JBS plant is already reeling as nearly 1000 workers stay home and others are presumptively positive for the illness.

CoBank regularly updates its forecasts and just released a spring outlook for the health of the agribusiness sector. The report finds that agricultural retailers are on relatively firm footing as they prepare for spring and that “Ag retailers’ inventories of seeds, agrochemicals, and fertilizer should meet customer needs during the 2020 planting season, which is expected to see an expansion in planted corn and soybean acres.”