In rural Colorado and across rural America, residents understand all too well the problematic lack of access to two major “B’s:” broadband and banking. While much ink has been spilled discussing high-speed broadband and wireless services, less has been used to address the growing lack of banking services in rural communities.

We’ve all seen it. With the decline of rural Mainstreets in the last few decades has come a decline in community banking. Locally-chartered banks have been closing or merging at an alarming rate–in fact, it’s at the highest level it has been in many years, and that keeps things changing for rural branches as well as those in urban and suburban communities. It’s not unusual for the name brand of one of your local branches to have changed several times in the last few years.

Closures Are Here to Stay

The closure of individual branches has accelerated in the last couple of years, due to both ongoing trends and the coronavirus pandemic. In fact, banks have been shuttering retails branches at a record clip, squeezing the availability of retail banking services in some small and rural communities across the nation.

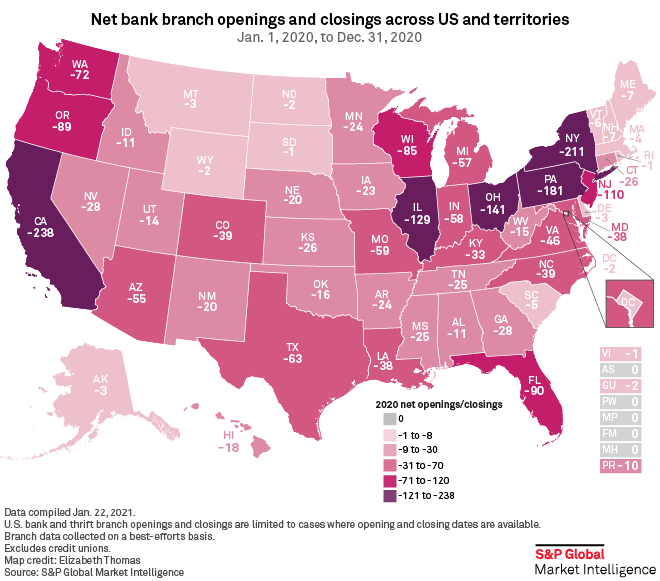

Banks closed 3,324 branches nationwide in 2020 and opened 1,040, according to S&P Global Market Intelligence data for a net decrease of 2,284. Industry experts see that trend increasing throughout at least 2021.

The problem isn’t new. A report by the Federal Reserve in 2019 found that between 2012 and 2017, the number of bank branches operating in rural counties dropped by -14 percent, 5 percent higher than the rate of loss in urban counties. Four counties in Colorado — Saguache, Mineral, Conejos and Costilla were identified by the report as ‘deeply affected” meaning they lost more than 50% of bank branches in the same time period.

Between 2012 and 2017, there was also a substantial increase in the number of communities that contained no bank headquarters, the majority of which were rural.

When local branches close, it can be a problem for rural and small-town residents. Clients have to travel farther, and neighboring businesses can lose foot traffic, among other ripple effects. Many older residents lack the technical ability to use online banking services. For agricultural communities, the unique nature of ag finance can make online banking difficult to conduct. And the lack of the other “B,” (reliable broadband and wireless communications) can prevent bank clients from having access to online banking. If you don’t have a signal, you cant check your balance.

The problem of the two “B’s” is a real and growing one for rural America. Lack of broadband and wireless services compound the lack of retail banking services, forcing consumers to use higher-cost and risky financial tools like check cashing services and payday loans.

Membership Matters

Colorado (CFB) and American Farm Bureaus are working to help alleviate the problem. The organizations are pushing hard to address the lack of investment in rural broadband and wireless services. CFB has created a partnership with Crown Castle, a wireless and broadband services developer to help advocate for the further buildout of robust communications infrastructure in areas of importance to the organization’s membership.

Colorado (CFB) and American Farm Bureaus are working to help alleviate the problem. The organizations are pushing hard to address the lack of investment in rural broadband and wireless services. CFB has created a partnership with Crown Castle, a wireless and broadband services developer to help advocate for the further buildout of robust communications infrastructure in areas of importance to the organization’s membership.

CFB is also working to advance new public investment and legislation that will provide increased funding for rural broadband services across the state.

And finally, Fam Bureau Bank is working to stand in the gap between consumers and the growing number of shuttering local bank branches. The online institution is a Fam Bureau company that understands rural communities and the unique banking needs of farmers and ranchers. Farm Bureau members can receive specialized services and perks by using their membership in Colorado Farm Bureau. To find out more, visit Farm Bureau Bank.