By Gus Gill, CFB Intern

While the impacts of COVID-19 continue to affect our local and state economies, representatives of CoBank’s Knowledge Exchange Division (KED) shared some much-needed optimism concerning our nation’s ethanol industry in a recent market update. To corn producers across the country, this is very good news.

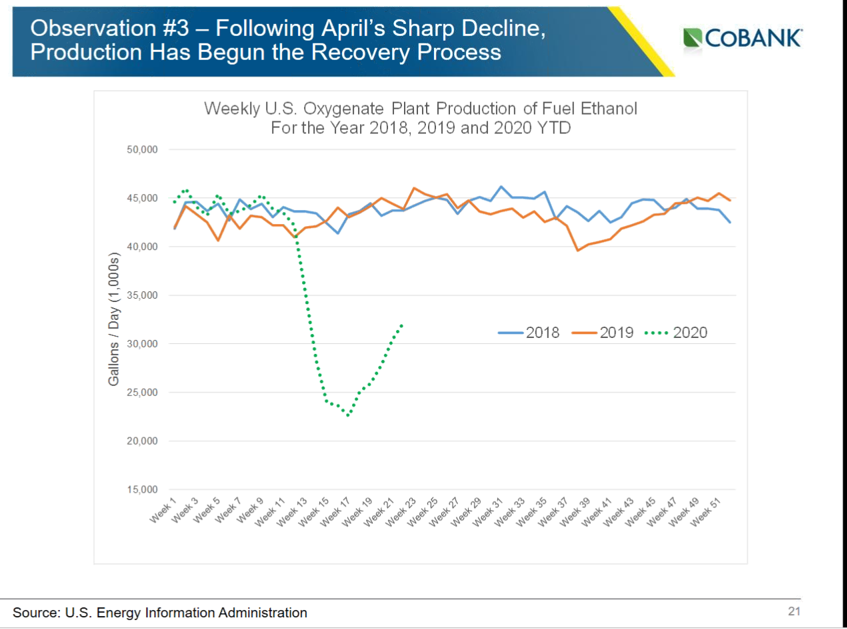

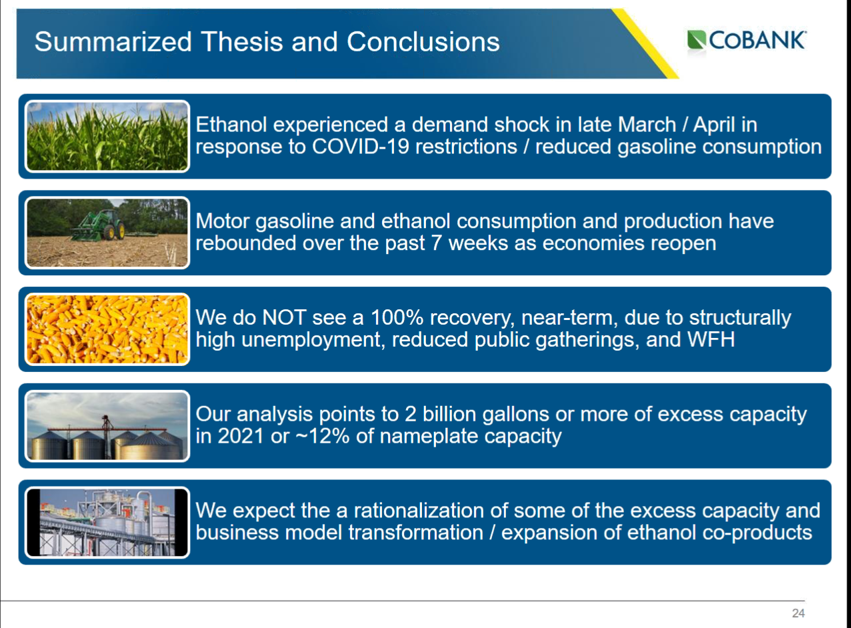

Following April’s very sharp decline in ethanol production, we are now in the midst of a recovery phase. Tanner Ehmke, manager of the KED, discussed how corn prices are beginning to rebound as a result of ethanol demand waking up out of the ‘COVID Coma’ over the course of the last seven weeks.

Although the analysts at CoBank are skeptical of seeing a 100% recovery in the next 18 months, they do anticipate production will return to at least 90% of its pre-COVID levels. “We should celebrate the fact that the industry has dealt with this difficult period and production has started to come back,” says Ken Zuckerberg, Lead Economist with CoBank.

Moving forward, the next steps for many ethanol producers will involve investing time and resources towards restructuring their business models. Currently, it is projected that there will be upwards of two billion gallons of excess capacity (i.e., the total productive capacity of ethanol producers minus actual ethanol demand) in 2021. As a result, we will likely see ethanol plants making efforts towards decreasing this forecasted excess capacity and expanding their production of ethanol co-products. “Ultimately, I think we will have a much stronger and healthier sector after this,” states Zuckerberg.

In these uncertain times, we will take every victory we can get. This promising outlook on ethanol and corn is a rallying point for agriculture, and we hope to see more positive stories like this for our industry in the weeks and months to come.

Additional reports and resources are available at CoBank’s Knowledge Exchange Division.